Understanding PCP Car Financing: Your Guide to Smarter Car Ownership

Are you considering a new car and exploring your financing options? Perhaps you’ve encountered the term “PCP car financing” and are wondering what it entails. Personal Contract Purchase (PCP) is a popular and flexible way to finance a vehicle, offering lower monthly payments compared to traditional loans. This article will delve deep into the intricacies of PCP car financing, demystifying its structure, benefits, and potential drawbacks to help you make an informed decision about your next automotive purchase. We’ll cover everything from how PCP works to key considerations you should keep in mind.

What is PCP Car Financing?

PCP car financing is a type of loan agreement specifically designed for purchasing a vehicle. It differs from a standard hire purchase agreement in how the total cost of the car is calculated and paid off. With PCP, you pay monthly installments over a set term, but these payments are significantly lower because they don’t cover the entire price of the car. Instead, your monthly payments cover the depreciation of the car – the difference between its initial value and its estimated guaranteed future value (GFV) at the end of the contract. This GFV is a pre-determined amount, essentially a minimum value the finance company guarantees the car will be worth.

Key Components of a PCP Agreement

To fully grasp PCP car financing, it’s crucial to understand its core components:

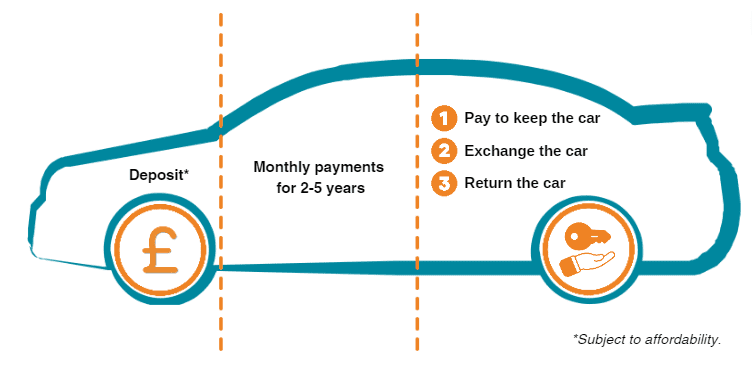

- Deposit: This is the initial amount you pay upfront, which can be a fixed sum or a percentage of the car’s price. A larger deposit typically leads to lower monthly payments.

- Monthly Payments: These are the regular installments you pay over the agreed contract term (usually 2-4 years). They are calculated based on the car’s depreciation, not its full purchase price.

- Guaranteed Future Value (GFV): Also known as the final balloon payment, this is the pre-agreed minimum value of the car at the end of the PCP contract. It’s based on factors like mileage, condition, and the car’s make and model.

- Contract Term: This is the duration of your PCP agreement, typically ranging from 2 to 4 years.

How PCP Car Financing Works

The process of PCP car financing is designed to be straightforward, yet it offers distinct advantages for car buyers. Here’s a breakdown of the typical journey:

You begin by choosing a car and agreeing on its price with the dealership. You’ll then pay an initial deposit, followed by monthly payments for the duration of your contract term. These payments are calculated to cover the anticipated depreciation of the vehicle over the contract period. At the end of the term, you’ll have three main options regarding the car:

- Return the car: If you’ve kept up with your payments and adhered to the mileage and condition clauses, you can simply hand the car back to the finance company. You will not owe any further payments, provided you haven’t exceeded the agreed mileage or damaged the vehicle beyond normal wear and tear.

- Part-exchange the car: You can use any “equity” you have in the car (the difference between its actual market value and the GFV) as a deposit for a new vehicle, potentially with the same dealer.

- Pay the GFV: If you wish to keep the car, you can pay the GFV amount. This final payment, often referred to as the balloon payment, will make you the outright owner of the vehicle.

PCP agreements often include mileage restrictions. Exceeding these limits can result in excess mileage charges at the end of the contract.

Advantages of PCP Car Financing

PCP car financing has gained popularity due to a number of compelling benefits:

- Lower Monthly Payments: As mentioned, your monthly payments are lower because you’re not financing the entire car price. This can make driving a newer or higher-spec car more affordable.

- Flexibility at the End of the Contract: The three options at the end of the term – return, part-exchange, or buy – provide significant flexibility, allowing you to adapt to changing needs or preferences.

- Access to Newer Cars: Lower monthly costs can enable you to drive a newer model or a car with a higher trim level than you might be able to afford with traditional financing.

- Fixed Costs: PCP agreements often include servicing and maintenance packages, helping you budget for predictable running costs.

Disadvantages and Considerations

While PCP offers advantages, it’s essential to be aware of potential downsides:

- You Don’t Own the Car Until the End: Until you pay the GFV, you are not the legal owner of the car; you are essentially hiring it.

- Mileage Restrictions: Exceeding the agreed mileage can lead to substantial charges, significantly increasing the overall cost.

- Condition of the Car: You’ll need to maintain the car in good condition, as excess wear and tear can also incur charges when you return it.

- Total Cost Can Be Higher: If you plan to keep the car and pay the GFV, the total amount paid, including interest and the final payment, might be more than if you had taken out a traditional loan.

| Scenario | Monthly Payment | End of Contract Options |

|---|---|---|

| PCP Financing | Lower | Return, Part-Exchange, Buy (GFV) |

| Hire Purchase | Higher | Own vehicle after final payment |

| Leasing | Low | Return vehicle only |

PCP vs. Other Financing Options

Comparing PCP to other popular car financing methods highlights its unique position. Hire Purchase (HP) involves paying off the entire car price, leading to higher monthly payments but outright ownership at the end. Leasing is similar to PCP in that you don’t own the car, but you typically don’t have the option to buy it at the end, and mileage allowances can be stricter. PCP strikes a balance, offering lower monthly payments than HP while providing the option to own the car, unlike traditional leasing.

Always read the full terms and conditions of any PCP agreement before signing. Understanding the GFV, mileage limits, and excess charges is crucial.

Frequently Asked Questions about PCP Car Financing

1. What happens if I want to end my PCP agreement early?

Most PCP agreements allow for early settlement. You’ll typically need to have paid off at least 50% of the total amount financed. You can usually settle the outstanding balance or part-exchange the car. Be sure to check your specific contract for early termination clauses and potential fees.

2. Can I customize my car if I have a PCP finance agreement?

While you can make minor cosmetic changes, significant alterations or modifications that affect the car’s value or originality are generally discouraged and may be prohibited by the finance agreement. If you plan on extensive modifications, PCP might not be the right choice.

3. What is considered “excess mileage” or “excess wear and tear” in a PCP agreement?

Excess mileage is any mileage driven over the pre-agreed annual mileage limit stated in your contract. Excess wear and tear refers to damage to the car beyond what would be considered normal for its age and mileage. This can include dents, scratches, stained upholstery, or damaged tires. Finance companies provide ‘condition guidelines’ to help you understand what is acceptable.

Conclusion

PCP car financing presents a compelling option for drivers seeking lower monthly payments and the flexibility to change their car regularly. By understanding the structure, key components, and your options at the end of the contract, you can leverage PCP to your advantage. Remember to carefully consider your driving habits, the car’s condition, and your long-term plans before committing. Thoroughly reviewing the agreement and seeking professional advice if needed will ensure you make a financially sound decision. Ultimately, PCP can be a smart way to drive a new car more affordably and with evolving choices at your fingertips.